ACT is a voluntary initiative of the UNFCCC secretariat Global Climate Agenda supporting corporate climate accountability. It develops sectoral methodologies as an accountability framework to support companies with delivering low carbon transition strategies and actions aligned with the Paris Agreement mitigation goal. An ACT assessment provides companies with a feedback report outlining best practice and opportunities for improvement and a rating to track progress. ADEME, the French Agency for Ecological Transition, and CDP, co-founded the initiative in 2015 at COP21. More about the co-founders here.

ACT is a registered trademark in the EU and UK.

Launched at COP21, ACT responds to the need for:

- A forward looking approach to decarbonisation, beyond carbon accounting, to assess how the private sector’s climate actions contribute to “hold the increase in the global average temperature to well below 2°C above pre-industrial levels” (Paris Agreement art.2).

- A framework to assess the relevance and trustworthiness of private sector public GHG emissions mitigation commitments

Ultimately, the objective of the ACT initiative is to drive climate action by companies and to help them align their strategies with low-carbon pathways.

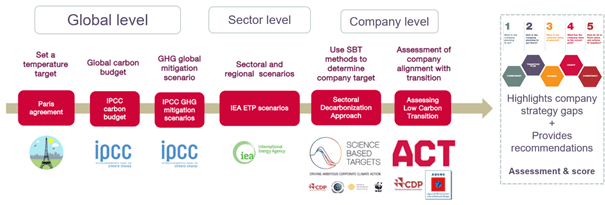

ACT builds on the Paris Agreement mitigation goal , and subsequent IPCC carbon budgets, and global mitigation scenario by using IEA sectoral and regional/national scenarios as decarbonisation pathways.

Any other relevant decarbonisation pathways can be used in the ACT tools for specific assessments. It assesses the gap between these low-carbon trajectories (or any trajectories that are of relevance from the assessment perspective) and the company’s trajectory. ACT assessments identify company’s strategy misalignments and provide recommendations, therefore closing the gap between corporate commitments and actions required to deliver a well-below 2°C economy.

With the ACT initiative, ADEME provides expertise with sectorial decarbonisation and transition challenges and international climate standards development, tools and training. It is also a major funder of the initiative.

CDP brings technical expertise and experience in environmental disclosure, benchmarking and climate change mitigation actions to the ACT initiative. It also engages its global network of companies and other stakeholders for them to share best practice and contribute to the developments of the initiative.

We consider the ACT pilot project phase as the time period between the launch at COP 21 in 2015 and the end of 2018. It aimed at:

- Identifying the key questions that need an answer to understand how companies contribute to the decarbonisation required to achieve the Paris mitigation goals

- Defining the process to develop sector specific methodologies to assess companies low carbon transition strategies against relevant sectoral decarbonisation pathways

- Developing and testing with companies three sectoral methodologies targeting three sectors with very different challenges when it comes to decarbonisation

- Testing methodologies with SMEs and mid cap companies using the French low carbon strategy (budget and pathways)

- Refreshing the draft methodologies (retail, electric utilities and automotive) and tools

The ACT Framework, the ACT Guidelines and the ACT electric utilities, automotive and retail methodologies result from the pilot project.

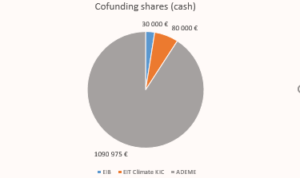

ADEME, EIB and EIT Climate KIC co-funded the ACT pilot project. The chart below outline their funding shares:

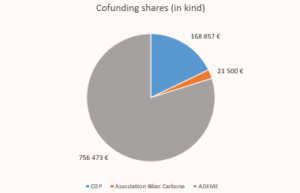

ADEME, CDP and Association Bilan Carbone made significant in-kind contributions as outlined in the chart below.

During the pilot project, an advisory group was formed of representatives of commercial and non-profit organizations and agencies working in the field of climate reporting. The advisory group was invited to comment on and review the methodologies via webconference and online at each stage of development.

Beyond ACT cofounders, partners included ClimateCHECK, 2° Investing Initiative and European Investment Bank.

Additionally, 21 companies volunteered to get an ACT assessment of their low carbon strategies with the existing historic ACT sectoral methodologies (auto, retail, electric utilities). Twelve completed their assessment. The ACT pilot report present the aggregated scores at sector level and key learnings.

Currently the ACT board includes the cofounders – ADEME and CDP – who lead on the ACT initiative strategy. The ACT secretariat is made up of dedicated staff from ADEME and CDP and external resources funded by EIT Climate KIC. The secretariat implements the initiative strategy set out by the board including steering Technical Working Groups and local councils.

Interested in joining the ACT governance? Contact us at info@actinitiative.org

CDP’s ratings, based on CDP disclosures, show company scores across those CDP topics a company responds to. These topics cover climate change, water security, forests (timber, palm oil, cattle products, and soy). Scoring methodologies aim at assessing how companies manage these topics against best practice and the related risks and opportunities.

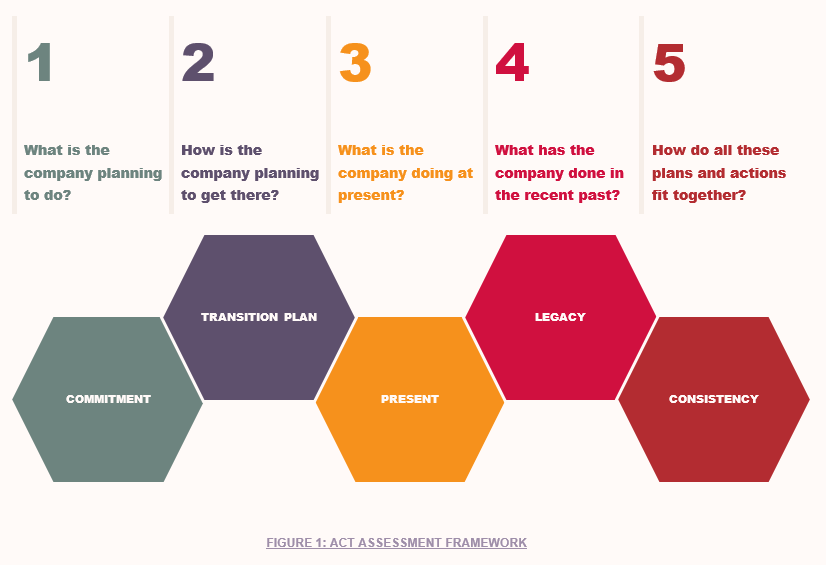

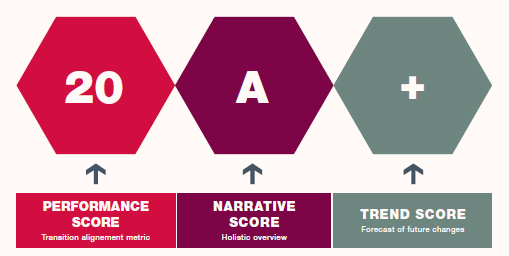

ACT’s ratings, based on ACT sectoral methodologies, show company scores across three dimensions: transition alignment metrics measured with KPIs (performance score ranging from 0 to 20), holistic overview of the assessment (narrative score from E to A) and forecast of future changes (trend score as +, – or =).

ACT methodologies assess how a company decarbonisation operations and strategy align with its individual decarbonisation pathway and the relevant sector’s low-carbon trajectory.

The ACT methodologies cover and primarily focus on transition risk exposure, rather than physical risk exposure, because the ACT methodologies aim to drive action by companies and encourage businesses to move to a well-below 2 degrees compatible pathway in terms of their climate strategy, business model, investments, operations and GHG emissions management. Transition risk is assessed through performance indicators such as those in the Management module, which assess the company’s oversight of climate change issues, low-carbon transition plan, and climate change scenario testing. The methodologies do also contain some performance indicators that assess data that can be relevant to physical risk exposure, such as a consideration of whether potential shocks or stressors have been assessed in company’s low-carbon transition plan.

In summary, the ACT methodologies build on the ladder that an organization follows towards reducing GHG emissions: measurement, transparent reporting and making public commitments to mitigate climate change. These practices mark the specific steps a company goes through when setting out to reduce its climate impact. Also, ACT relies on data TCFD advocates should be in the public domain through corporate reporting.

ACT methodologies are not develop for performance aggregation at portfolio level as underlined indicators and activity data used to calculate those indicators do not always match financial indicators used at portfolio level. ACT assessments and ratings are best used for companies climate engagement and benchmark comparison between companies within the same sector in a portfolio as well as for investors to promote, track and understand companies decarbonisation strategy and GHG reduction. This from an ACT initiative perspective is currently the only methodology with empirical evidence for financial institutions willing to contribute to GHG reduction in real economy.

The World Benchmarking Alliance’s Climate and Energy Benchmark operationalise the ACT methodologies to create freely, publicly available rankings of companies, giving each company a peer group comparison on how the industry is performing and contributing to a low-carbon economy and the sustainable development goals. Detailed information on a company’s performance, including a breakdown of their scores per module of the performance assessment and a written explanation of the narrative and trend assessments is made available to various stakeholders. WBA is updating its benchmarks on an iterative basis, adding further sectors until 2023.

The ACT assessments are used to create free, publicly available rankings in the World Benchmarking Alliance (WBA)’s benchmarks. WBA publish various benchmarks in high emitting sectors, including Automotive and Electric Utilities. More details about the WBA Climate nd Energy benchmarks can be found here.

Whenever possible, ACT uses the other initiatives as inputs, in order to be complementary. For example, in the ACT Transport Methodology, we use EU taxonomy to define what is a low carbon vehicle. From conception, ACT has learned from and aligned with a wider set of standards. The ACT Framework contains methodology implementation principles, which draw on GRI, IIRC, SASB, Arista 3.0, and the ISO 14064-1 and GHG Protocol principles. Many of the ACT indicators capture information required or recommended to be reported in the CDP, GRI, SASB and Taskforce on Climate-related Financial Disclosure (TCFD) frameworks. In particular, the Management module of the ACT methodologies, which contains indicators on the company’s oversight of climate change issues, climate change oversight capability, low-carbon transition plan, climate change management incentives, and climate change scenario testing shows convergence with the disclosures recommended by the TCFD.

To date ACT Assessment methodologies cover the following sectors:

- Retail

- Electric Utilities

- Automobile Manufacturing

- Real Estate

- Property Development

- Construction

- Oil & Gas

- Cement

- Transport (passenger & freight, all modes)

A Generic methodology enables ACT assessment of companies activites which are not covered by sector specific methodologies. It covers mining & quarrying, manufacturing, wholesale, public works and infrastructures, services with high or low GHG impact.

By September 2021 Agriculture and Agro food as well as Iron and Steel will be covered. By March 2022, Chemicals, Glass, Aluminium and Pulp and Paper will be covered.